So – you and your better half are thinking about buying a house. Congrats! You have a ballpark idea of what’s what – home inspections, down payments, offer letters, and credit scores – but that last one is throwing you for a loop. After all, there are two people purchasing the house how do two credit scores factor into the homebuying equation? Do they take the higher number? Do they average them? What if you aren’t married yet?

For all your questions, we say: relax. There might be more than one piece to the puzzle, but we’ll show you where they fit. Here’s what you should know about the credit scores of you and your partner.

Two Credit Scores, Buying One House. How?

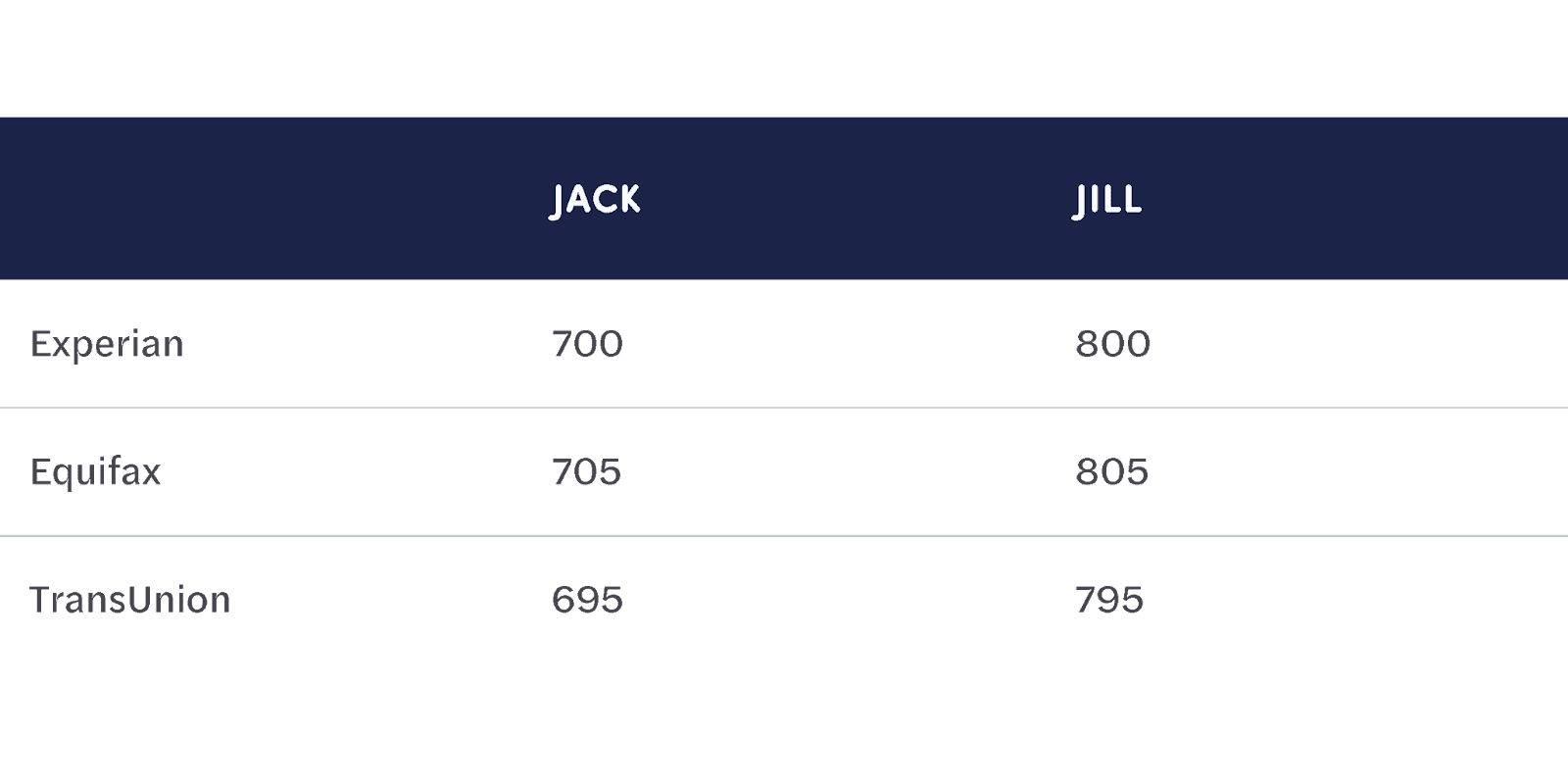

Unlike tax returns, your credit score stays linked to you and you alone – there is no joint option. So, when a couple applies for a loan, the lender will look at both of their scores. A good way to visualize this is:

Depending on the type of mortgage (as well as the lender), the lender will typically use the lowest middle score between you and your partner. So, if you’re Jill (795, 800, 805), and your spouse is Jack (695, 700, 705), your loan amount and interest rate will potentially be dependent on the score of 700. But – it never hurts to check with your loan provider to ensure you’re taking advantage of a loan program that works with your credit scores.

What If We’re Not Married Yet?

Doesn’t make one bit of difference! Credit scores reflect the individual’s credit and marital status has no direct bearing on your credit. You could theoretically buy a house with your college roommate! Dorm-life has a certain (albeit rose-tinted) charm.

What If One of Our Credit Scores is Less-Than-Ideal?

You can choose to drop the individual with the lower score from the application. Depending on the state that you’re looking to buy, lenders may not have to consider your partner’s credit profile if they’re not on the loan, except in the case of foreclosure/bankruptcy. If one of you has a high enough credit score to qualify by yourself, then great!

These were just a few of the most common FAQs we’ve encountered – chances are, you might have some additional follow-up questions that we didn’t cover. Don’t worry, we have you covered. This is where our trusted lending partner Atlantic Coast Mortgage really shines. They’ll not only help you navigate the mortgage process, but they’ll also make sure your mortgage financing experience is simple, easy, and stress-free. Have questions? Reach out to them today!